The Value Proposition of Private Markets - Outperformance and Diversification

An iAccess Partners Series: Episode 2/6

In our first episode, we explored how Private Markets have grown from a niche “alternative” allocation into a $13 trillion asset class. We saw that Private Markets now account for roughly 71% of global equity capital raised, eclipsing public markets in both scale and scope.

Today, we turn to the core question for every investor: What do Private Markets deliver in terms of performance and risk mitigation opportunities? In this episode, we’ll compare Private Markets returns against public benchmarks, unpack the drivers behind their outperformance, and demonstrate how Private Markets can enhance portfolio diversification.

Key takeaways: Episode 2/6

1. Private Markets have outperformed public benchmarks by 3-6% annually over the past decade – across all asset classes.

2. Four key drivers – active value creation, alignment of interests, long-term focus, and strict investment selection processes – explain Private Markets' historical outperformance.

3. Diversification benefits arise from longer investment horizons compared to public markets, low correlations with traditional public assets, and valuations less impacted by daily market sentiment.

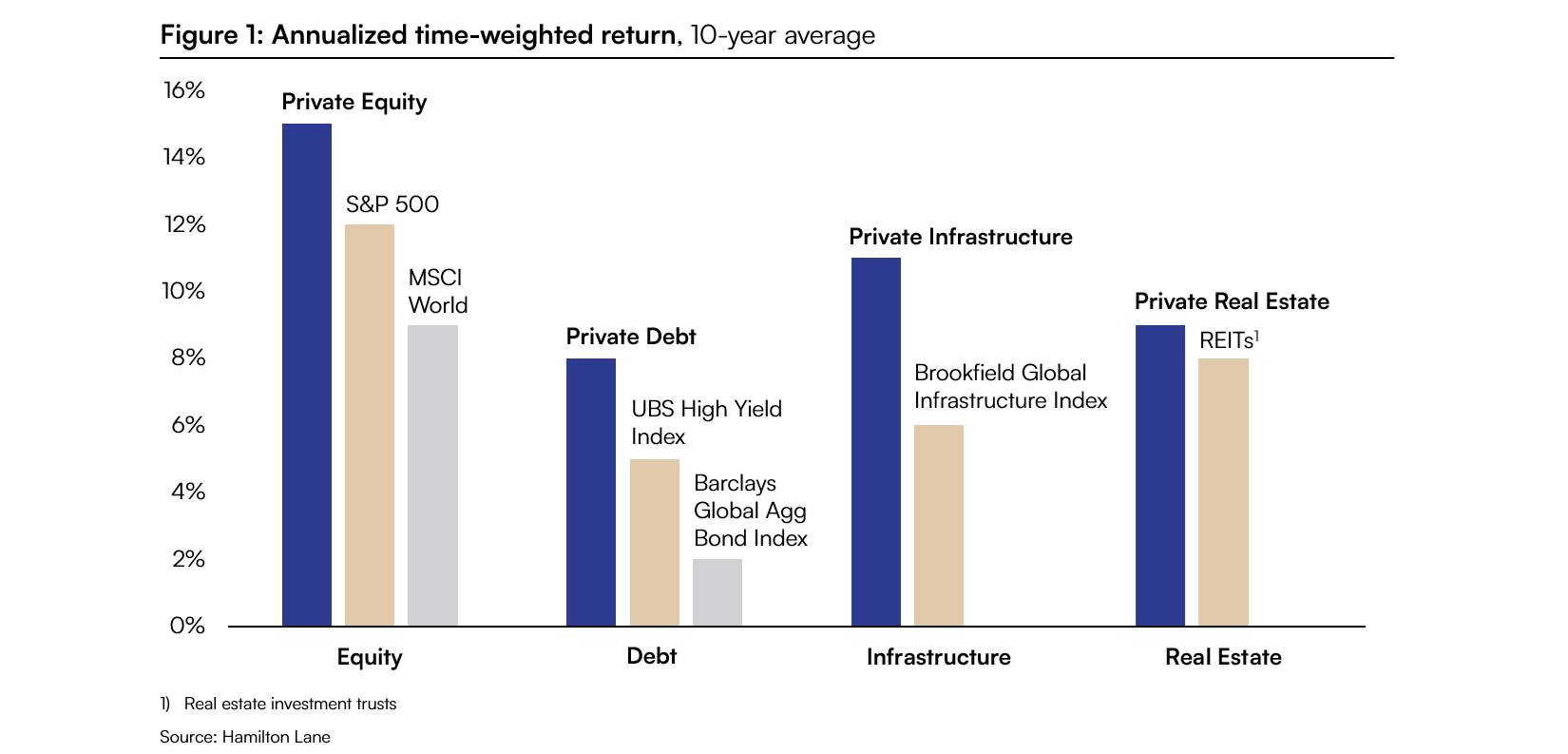

Private Markets vs. public markets: A history of outperformance

Decades of data show that Private Markets have consistently rewarded investors with higher long-term performance than traditional public market investments. This outperformance pattern holds across market cycles – even during recessionary periods. Moreover, the outperformance is evident across all four asset classes; equity, debt, infrastructure, and real estate. As figure 1 illustrates, global Private Equity has generated 15% in annualized returns over the past decade, versus 12% for the S&P 500 and 9% for MSCI World, which tracks large‑and mid‑cap public stocks across all developed markets globally. Notably, that 9% return of the MSCI World, one of the most popular global investment vehicles for private investors, closely matches the returns observed in Private Debt and Private Real Estate, despite the lower risk measures of these asset classes. Therefore, investors in Private Debt and Real Estate have historically achieved similar returns as public equity at lower risk levels.

Digging deeper into Private Debt reveals a remarkable track record; it has outperformed its public peers for 23 consecutive years. Middle-market direct lending alone has delivered 5-6 percentage points higher yield than high-yield bonds, while maintaining similar default rates. Private Real Estate and Private Infrastructure have also delivered robust returns. Over full market cycles, these asset classes has achieved equity-like returns but at significantly lower volatility than listed equities.

What drives Private Markets' outperformance?

Several factors explain why Private Market investments often outperform their public market counterparts:

- Active value creation: In Private Markets, fund managers take an active ownership role to improve underlying assets. Often being a majority owner, Private Markets managers can be highly involved in operational and strategic decisions, driving value creation. This hands-on approach accelerates operational improvements and growth, contributing directly to higher investor returns.

- Alignment of interests: Fund managers typically closely tie compensation of the executive team and key roles in their investments to multi-year results, creating a strong alignment of interest between the owner and the management.

- Long-term focus and illiquidity: Private businesses are more insulated from quarterly earnings pressure and daily stock volatility given their illiquidity, allowing them to prioritize fundamental value creation over short-term profits. This resulted in the so-called “illiquidity premium”, a return upside expected by investors allocating funds to less liquid assets such as Private Markets.

- Strict investment selection and deal structuring: As discussed in episode 1, the universe of Private Markets is far larger than the public markets. This means fund managers can be highly selective in identifying promising investment opportunities and negotiate investments on favorable terms.

In summary, Private Markets' outperformance stems from a combination of hands-on value creation, the alignment of interest between owners and managers, a long-term focus, and highly diligent investment selection. These factors have allowed private asset classes to deliver excess returns, attracting qualified investors to continue allocating to Private Markets.

Diversification benefits: Smoother returns and lower correlation

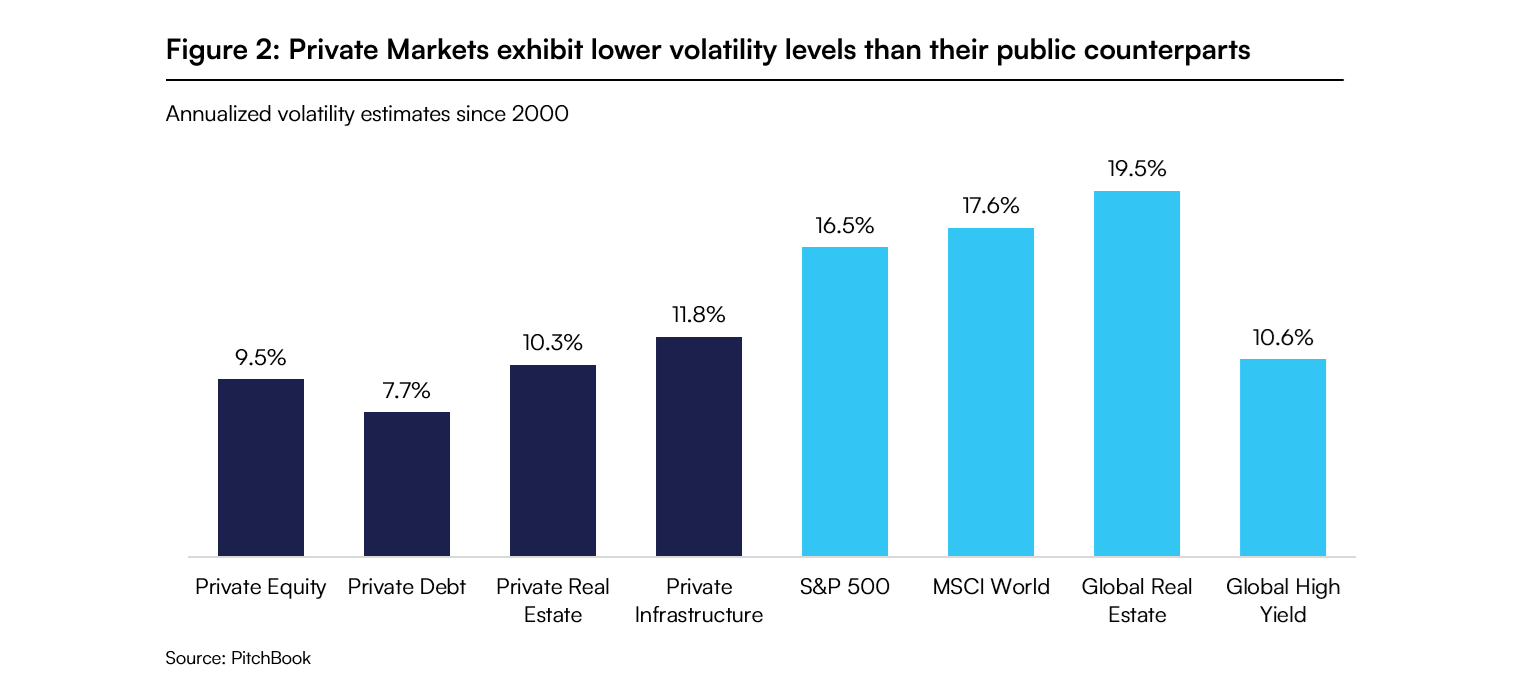

Beyond higher returns, Private Markets offer powerful diversification benefits. The addition of Private Markets has been shown to significantly reduce portfolio volatility. This pattern is evident across asset classes, as shown in figure 2.

Moreover, Private Markets have historically weathered crises better than their public equivalents – losses in Private Equity and Private Debt during the dot-com bubble, the 2007/8 financial crisis, the 2020 COVID-19 pandemic, and the post-pandemic turbulences were much more muted than the sharp crashes seen in public stocks and bonds (see figure 3).

What makes Private Markets more resilient during periods of heightened volatility?

In part, private assets are better insulated from short‑term volatility because they are less influenced by daily price fluctuations and the market sentiment that often drives public markets. This means that during times of crisis, fund managers can navigate downturns strategically without being forced to exit positions, maintaining a long-term focus. In fact, some of the best‑performing Private Equity vintages began during recessions, demonstrating how managers can capitalize on dislocations that public markets often miss.

Another source of resilience and predictable portfolio performance comes from recurring income streams generated by Private Debt, Private Real Estate, and Private Infrastructure. These distributions reduce reliance on valuation gains and eliminate the need to “time the market” as investors earn returns through ongoing cash yields.

The bottom line: Restoring diversification with Private Markets

The traditional 60-40 portfolio of 60% public stocks and 40% bonds has become less effective as a diversifier in recent years. Stocks and bonds, which historically moved in opposite directions, have been moving more in tandem (higher correlation) in recent years. For instance, both U.S. stocks and core bonds fell simultaneously in 2022, undermining the 60-40 hedge.

By allocating a proportion of your overall portfolio to Private Markets, you introduce new return drivers that are not as correlated with either equities or bonds, helping to restore diversification and potentially achieving higher returns with lower overall volatility.

Up next: The allocation gap: Private investors vs. institutions?

Despite these clear benefits, private investors remain far less allocated to Private Markets compared to institutional investors. This gap highlights how individual investors are missing out on the same structural advantages and performance drivers that institutions have captured for decades.

In our next episode, we will examine this allocation gap in detail – comparing institutional and private investor allocations across Private Equity, Private Debt, Real Estate, and Infrastructure, and tracking how these allocations have evolved over time.

Interested to learn more? Discuss Private Markets with iAccess Partners

-

-